Savings, Spending, and Jobs Get US to Necessities, Conveniences, and Amusements

February 1, 2023

After two years of pandemic pent-up demand, our increased savings are now entering the economy as spending on what Smith calls “necessities, conveniences, and amusements.” Parrish and Yancy walk us through the data to help us understand the current trends.

After two years of pandemic pent-up demand, our increased savings are now entering the economy as spending on what Smith calls “necessities, conveniences, and amusements.” Parrish and Yancy walk us through the data to help us understand the current trends.

In our previous posts we looked at the causes and consequences of the Great Resignation as well as factors that influence whether increased US savings will catalyze investments and lead to economic growth or whether those savings will be consumed by inflation. Here’s where we ended:

“So, we can see the savings and we can see the investments but we don't know how much of the investment is coming from the savings. There are other possibilities for the sources of the investments like profits from raising prices or loan financing. BUT to the extent that the savings are leading to investments, we can look toward higher rates of economic growth in the future.”

What have we learned and how can Adam Smith help us think a little more clearly about our modern economic questions and challenges?

The Numbers

Adam Smith’s states, “Every man is rich or poor according to the degree in which he can afford the necessities, conveniences, and amusements of human life.”(WN, Chapter 5) If the money ends up being used up by higher prices caused by inflation, people are poorer in their ability to purchase even if they have more dollars.

Here are the pieces we need to look at:

1) Spending

2) Investment

3) Growth in the Economy (GDP)

4) Employment

5) Inflation

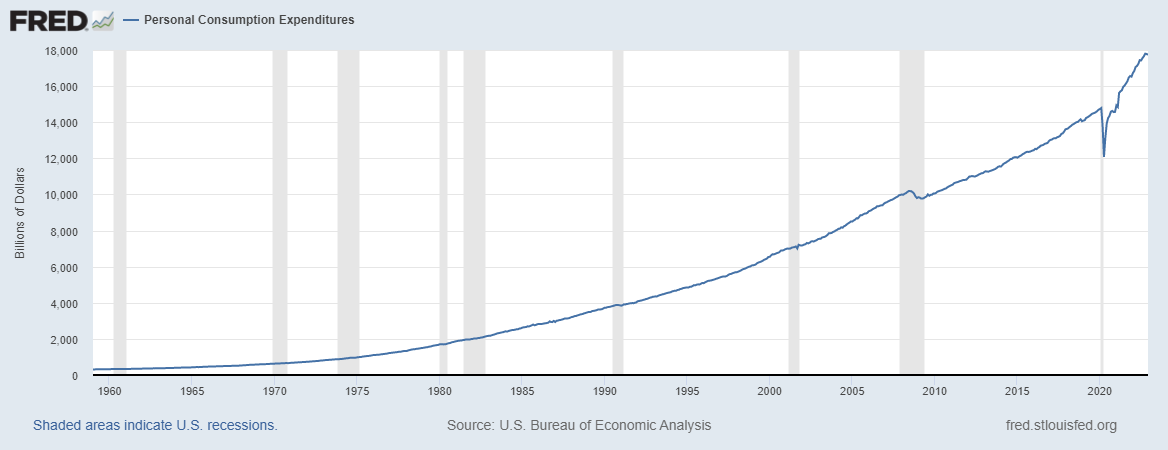

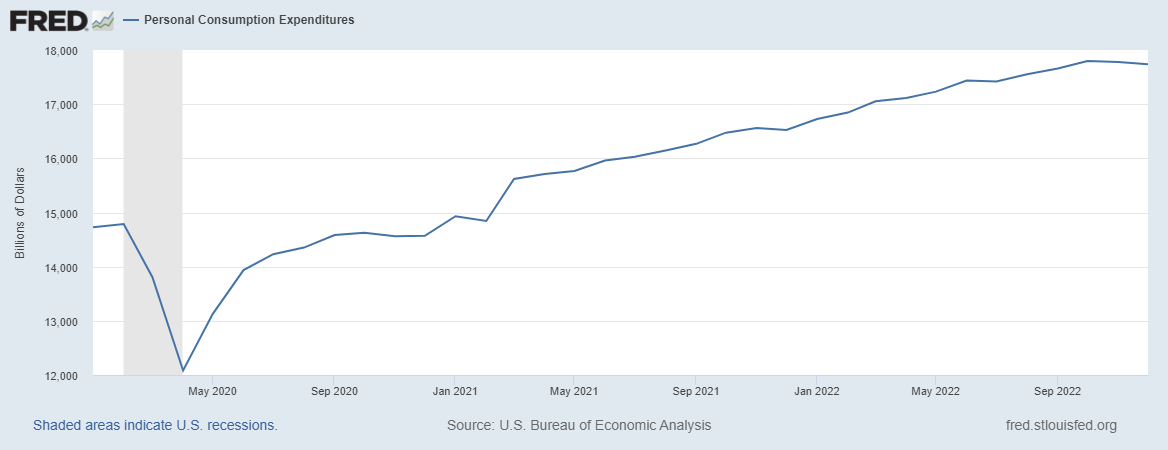

After two years of pandemic pent-up demand, our increased savings are now entering the economy as spending on what Smith calls “necessities, conveniences, and amusements.” Since our previous posts personal income, disposable income, and personal consumption have all increased. Here’s just the personal consumption. Long-term is first; more recent data is after. You will notice that the personal consumption expenditures and domestic investment are not inflation adjusted but we will talk more about the impact of inflation later in the piece.

Long-term personal consumption expenditures

Source: https://fred.stlouisfed.org/graph/?g=ZhpF

Recent personal consumption expenditures

Source: https://fred.stlouisfed.org/graph/?g=ZhqW

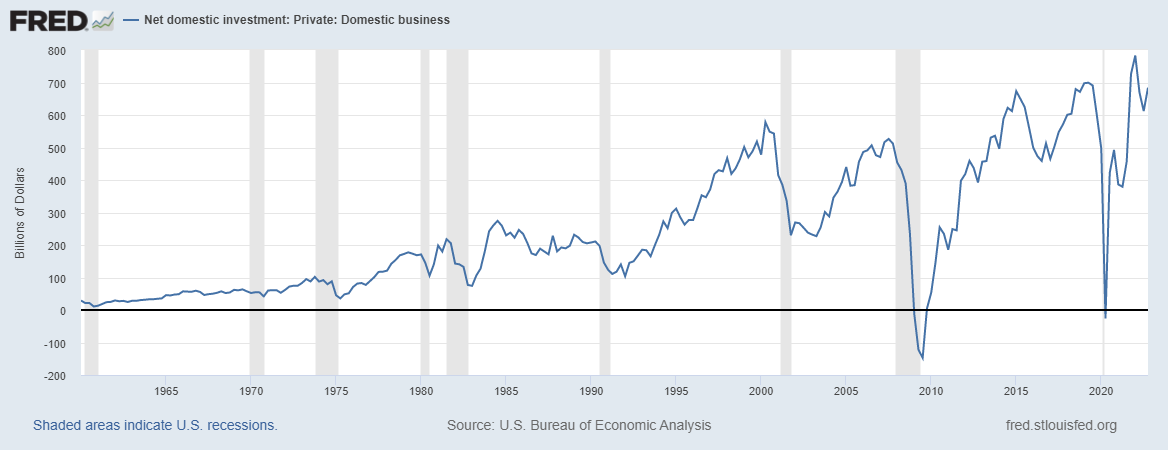

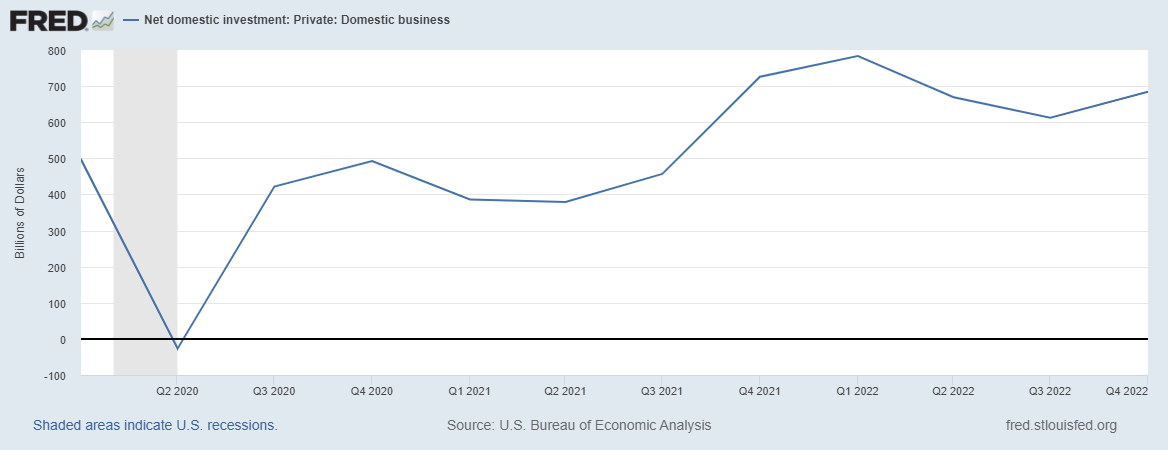

Investment is still high. Long-term first; more recent data after.

Long-term domestic investment

Source: https://fred.stlouisfed.org/graph/?g=Zhvc

Recent domestic investment

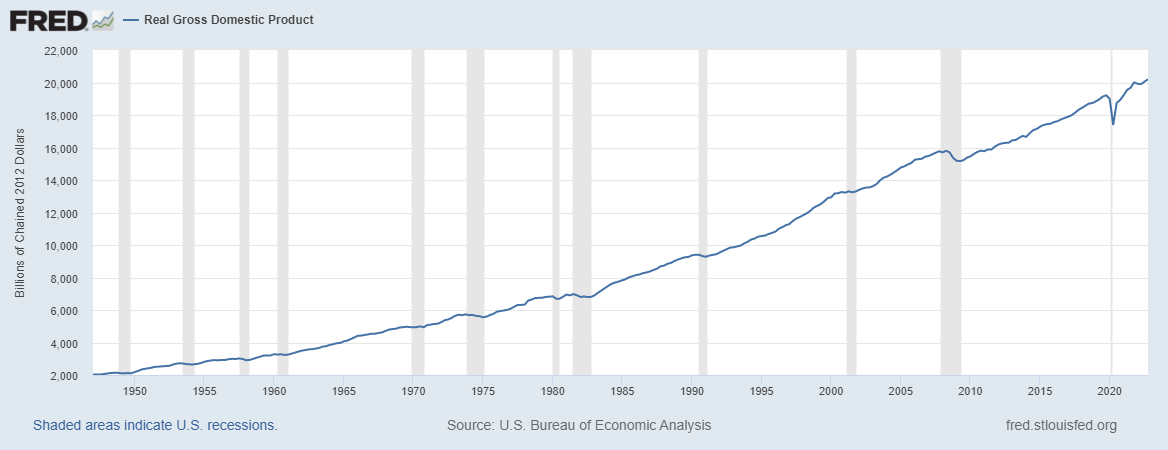

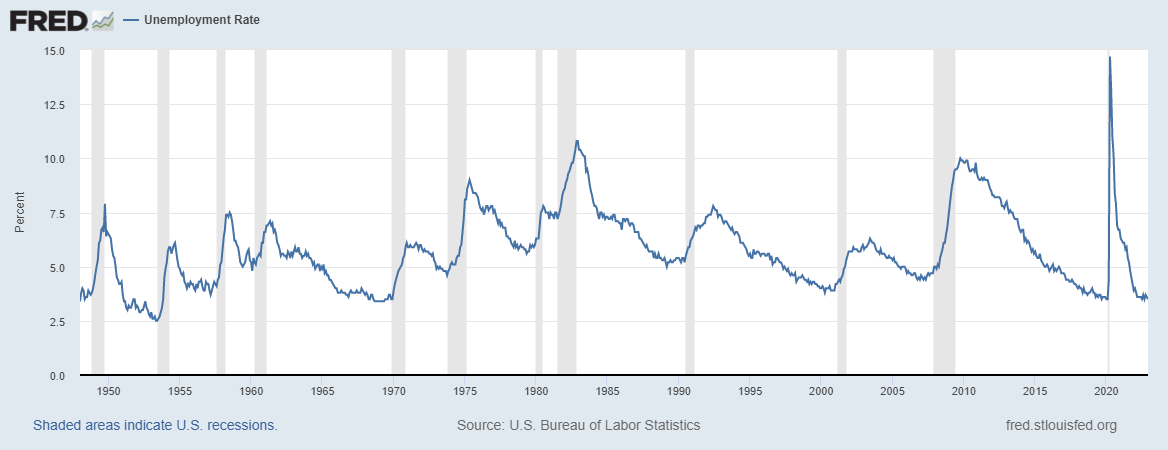

The economy is expanding and unemployment is decreasing.

Long-term GDP

Source: https://fred.stlouisfed.org/graph/?g=Zhtm

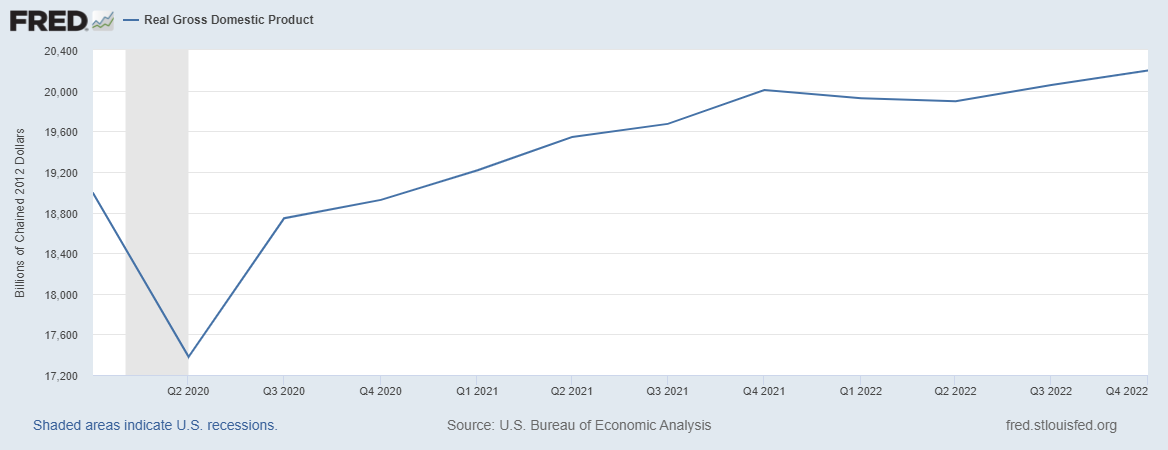

Recent GDP

Source: https://fred.stlouisfed.org/graph/?g=ZhtK

Long-term unemployment rate

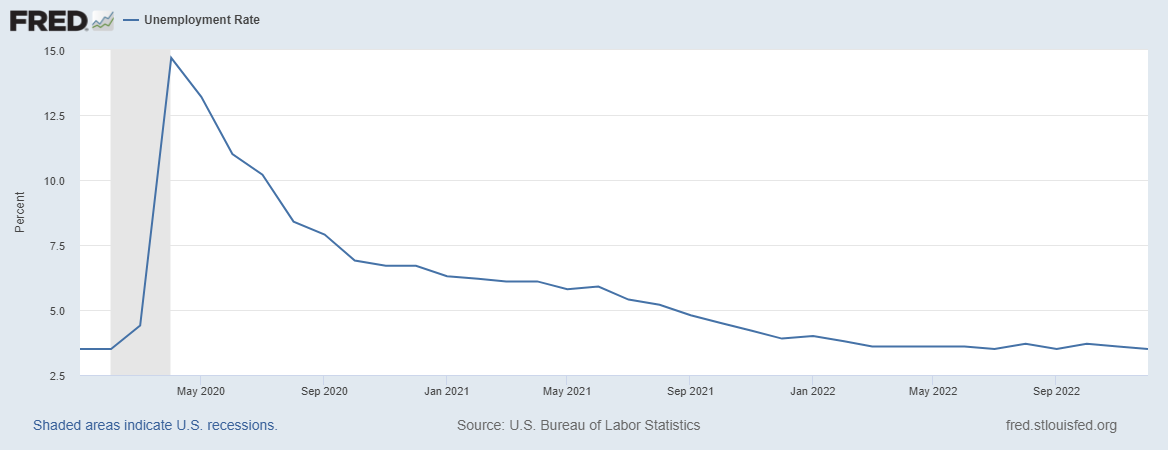

Recent unemployment rate

So far, these numbers are all heading in the right direction. But now we need to talk about inflation. It is not surprising to see unemployment decreasing and inflation increasing. They typically have this inverse relationship. But with inflation so high for so long, the US Federal Reserve’s will use its influence. One of the Federal Reserve’s mandates is to keep inflation rates low and stable.

To hedge against worsening inflation and bring down the inflation rate, the Federal Reserve has increased the Effective Federal Funds Rate (EFFR), in order to accommodate a Target Rate Range of 3.75 to 4.00, from a pandemic low of November 2020 of 0.09% to the most recent high on December 12, 2022 of 3.83%. (We especially like this interactive graph to help increase our and our students’ understanding: https://www.newyorkfed.org/markets/reference-rates/effr)

It is not surprising that the Federal Reserve is doing this but its goal and its effect is to heavily influence the behavior of individuals all over the world in a specific way.

What about the Invisible Hand?

The Great Resignation is not the only crisis in recent memory. Most of us (older than my high school students) remember well the Great Recession of 2008. In 2010, Stephen LeRoy, a professor emeritus at the University of California, Santa Barbara, and a visiting scholar at the Federal Reserve Bank of San Francisco (FRBSF), revisited Adam Smith’s claim that competitive markets are better poised to guide resources to their most highly-valued use than markets with large amounts of government interference. In his FRBSF Economic Letter of May 2010 on the tail of the Great Recession, LeRoy concluded,

The question is when and to what extent—not whether—private markets fail and therefore must be supplanted or regulated by government…it appears that current sentiment is less supportive of Adam Smith’s verdict on the efficiency of markets than was the case prior to the financial crisis.

It's easy to invoke Adam Smith but he can be a hard thinker to pin down and he’s certainly more nuanced and careful than some modern caricatures make him out to be. In An Inquiry into the Causes of the Wealth of Nations, Smith emphasizes that much policy is undesirable and yet, Smith acknowledges that governments are tasked with providing “publick works” and “publick institutions” for the good of the whole. (WN, Chapter 9). https://plato.stanford.edu/archives/win2020/entries/smith-moral-political/

Smith scholars Ryan Hanley and Maria Pia Paganelli in their paper, “Adam Smith on Money, Mercantilism and the System of Natural Liberty,” have their own view,

Smith’s critical analysis of what might be considered the proto-monetary policies [debasement, paper credit money, and tariffs] of his day, like his theory of money itself, is consistent with his view that social and economic growth is not the product of conscious design.” However, although Smith cedes “rational intervention” in the social order does not succeed, he does accommodate for “the science of a statesman or legislator” (WoN IV.Intro.1) in order to “promote the enrichment of the entire nation.

The Great Resignation is about a lot of individuals making microeconomic choices to leave or change jobs. However, the macroeconomic effect of these choices, in combination with other responses to the pandemic, led to increased government interventions in several areas. It’s safe to say that Smith would have cast a critical eye over many, perhaps even all these interventions, but also evaluated them on their outcomes as well as their stated purposes.

Conclusion

Adam Smith argued that, “Our ancestors were idle for want of a sufficient encouragement to industry.” (WN, Chapter 3) The Great Resignation can be seen as another example where workers without sufficient incentives will seek other jobs or even withdraw from the labor force. Reduced spending and government transfers to hedge against pandemic-induced income loss led to increased savings. Pent-up demand then began to be satisfied. Subsequent inflation heightened quickly as prices responded to such demand especially considering disruptions to supply chains. But the invisible hand has been through worse. Smithian insights can help us better understand and evaluate policies for now and in the future whether shocks come from pandemics or elsewhere.

Mentioned in this post:

- Federal Reserve Bank of New York, Effective Federal Funds Rate, Interactive Graph

- Stephen LeRoy’s “Is the “Invisible Hand” Still Relevant?”

- Ryan P. Hanley and Maria Pia Paganelli's “Adam Smith on Money, Mercantilism and the System of Natural Liberty”

Want to learn more?

- Maryann Keating, Adam Smith on Wage Taxes and Labor Force Participation

- Alex Aragona, Adam Smith on the Interests of Labor and Business

- Peter Foster’s Adam Smith Invisible Hand