What Would Adam Smith Think: Will US Savings Catalyze Investment?

August 29, 2022

We saw increased savings and decreased spending BUT will that led to the long-term growth we're used to seeing? Or is our current economic situation fundamentally different?

We saw increased savings and decreased spending BUT will that led to the long-term growth we're used to seeing? Or is our current economic situation fundamentally different?

This is part 2 of an article on Adam Smith and the Great Resignation. Here is part 1.

In our last post, we discussed Adam Smith’s insight that, “Our ancestors were idle for want of a sufficient encouragement to industry” and how the US labor market was and is providing “insufficient encouragement” in many cases. In other words, unhappy workers are producing less. More people are quitting more often and it’s unclear how long this trend will last. Here, we’ll focus on how increased savings will–hopefully–benefit the nation.

Saving catalyzes investment, usually.

In our last post, we discussed Adam Smith’s insight that, “Our ancestors were idle for want of a sufficient encouragement to industry” and how the US labor market was and is providing “insufficient encouragement” in many cases. In other words, unhappy workers are producing less. More people are quitting more often and it’s unclear how long this trend will last. Here, we’ll focus on how increased savings will–hopefully–benefit the nation.

Saving catalyzes investment, usually.

The pandemic and the responses to it incentivized more individuals and households to increase saving and decrease spending.

Increased savings

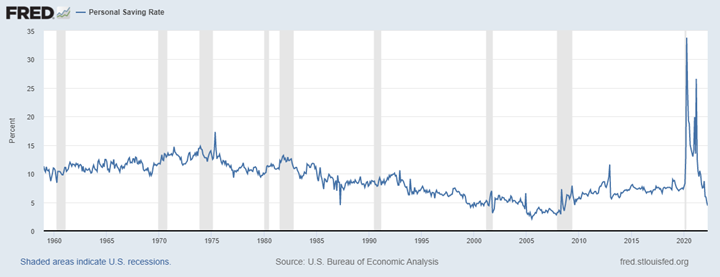

Long-term personal savings rate

Increased savings

Long-term personal savings rate

As you can see, it’s been decades since Americans have saved at such high percentages. The previous record American saving rate was 17.3% in May 1975, which was spurred by rocketing gas prices, government spending on the Vietnam War, and a Wall Street stock crash. Over the last 10 years, it has hovered in the 6-8% range.

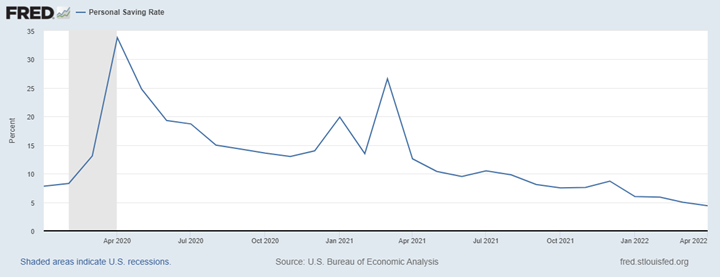

Then, we can take a closer look starting in March of 2020 (the same date range we looked at closely in Part 1 to understand the relationship to the spread of Covid-19 and responses to the virus). You can see that the 8% savings rate from January and February of 2020 jumps dramatically. Its height is at 33.7% in April of 2020. The savings rate did decline to approximately 14% in April 2021; however, the higher savings afforded time and possibility for dissatisfied workers to rethink job prospects.

Recent personal savings rate

Source: https://fred.stlouisfed.org/graph/?g=QiaS

It might seem obvious that increasing savings and decreasing spending would go together but let’s take a look at the relationship a little more closely.

Decreased spending

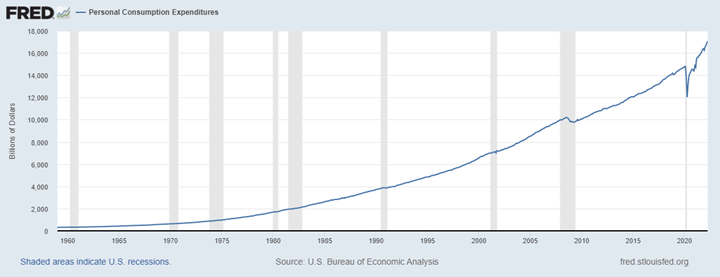

Once again, Here's the long term trend in personal spending first.

Long-term personal consumption expenditures

Source: https://fred.stlouisfed.org/graph/?g=Qi8O

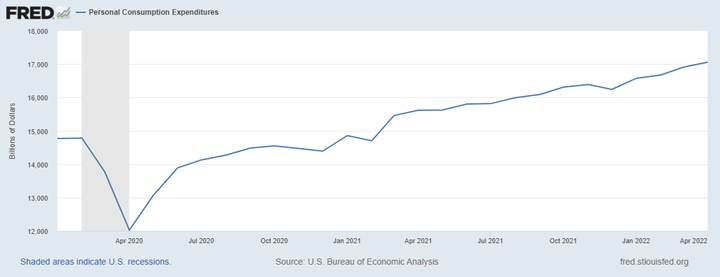

And here's zooming in to more recent dates:

Recent personal consumption expenditures

It might seem obvious that increasing savings and decreasing spending would go together but let’s take a look at the relationship a little more closely.

Decreased spending

Once again, Here's the long term trend in personal spending first.

Long-term personal consumption expenditures

Source: https://fred.stlouisfed.org/graph/?g=Qi8O

And here's zooming in to more recent dates:

Recent personal consumption expenditures

It’s clear in the data that spending is decreasing at the same time that savings are increasing as the pandemic and early responses to it are having large effects across the US. These actions may have differing catalysts–downturns in consumer spending due to job loss or shutdowns as well as uncertainty about the future but all incentivize stockpiling cash. But it’s important to remember that governments at different levels and many different agencies are all putting into place new policies or changing long-standing policies so it’s a unique environment that individuals are trying to navigate.

The Role of the Government

A June 2022 Federal Reserve report about bank deposit growth during the pandemic summarizes:

“[Households and businesses] were more likely to keep their savings in very liquid bank deposits rather than move their savings to illiquid assets, some of which would have then moved outside the banking system. In addition . . . the federal government began making stimulus payments to households in 2020 and 2021 through direct payments, extended unemployment supplementary payments, and augmented the child tax credit through legislation such as the CARES Act and the American Rescue Plan, which raised the incomes of many households. Likewise, through the paycheck protection program (PPP), the federal government made loans directly to small businesses that would be forgiven if those firms spent a certain portion of the funds on wages of employees. Moreover, many households were able to defer payments on mortgages and other debt during the pandemic period, which enabled them to keep more of their wages and stimulus payments as savings. As the stimulus payments were made, a wide swath of households across the economy received boosts to their deposit accounts.”

If these savings end up going to finance government debt in the future, it won’t lead to a higher rate of long-term growth (like increases in savings usually do). There are some reasons to be concerned about this. This article by Jospeh Politano, “Americans are Spending Their Excess Savings” goes into details (with thanks to Jeremy Horpedahl for the pointer) but a TLDR version is that a lot of excess savings are coming from government transfers and that money has to come from somewhere.

But if the savings aren’t eaten up by government debt, we can look forward to higher rates of long-term growth in the future. The more the corporate sector absorbs savings and turns them into investments, the more confident we can be that these savings will lead to higher rates of long-term growth. Let's look at what is happened with business investment next:

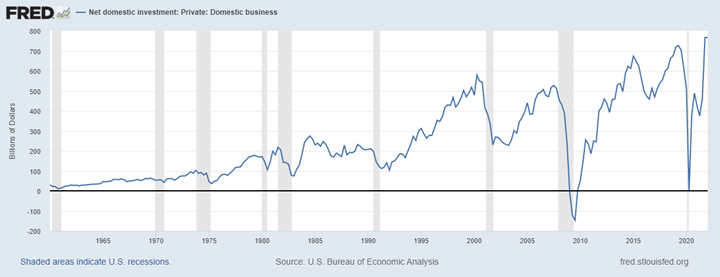

Long-term domestic investment

Source: https://fred.stlouisfed.org/graph/?g=R33W

Long-term domestic investment

Source: https://fred.stlouisfed.org/graph/?g=R33W

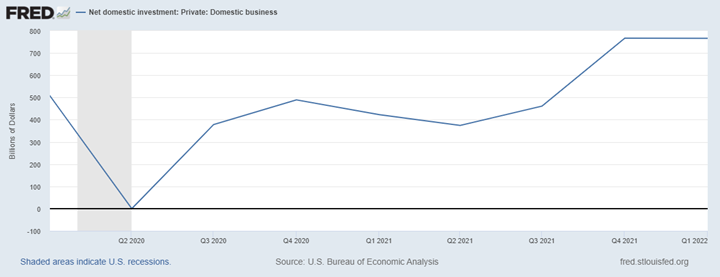

Recent domestic investment

https://fred.stlouisfed.org/graph/?g=R34f

So, we can see the savings and we can see the investments but we don't know how much of the investment is coming from the savings. There are other possibilities for the sources of the investments like profits from raising prices or loan financing. BUT to the extent that the savings are leading to investments, we can look toward higher rates of economic growth in the future.

So, we can see the savings and we can see the investments but we don't know how much of the investment is coming from the savings. There are other possibilities for the sources of the investments like profits from raising prices or loan financing. BUT to the extent that the savings are leading to investments, we can look toward higher rates of economic growth in the future.

Want to read more?

News stories that inspired the authors

- US savings rate hits record 33% as coronavirus causes Americans to stockpile cash, curb spending - CNBC

- What the ‘Great Resignation’ Means for the U.S. Economy | ABA Banking Journal

- Savings surge during the pandemic - Federal Reserve Bank of Kansas City

- The U.S. Saving Rate is Soaring | NextAdvisor with TIME

- 7 In 10 Americans Are Spending Their Savings Because Of Inflation – Forbes Advisor

- Stevenson discusses the Great Resignation and inflation | Gerald R. Ford School of Public Policy (umich.edu)

On related topics

- Steve Horwitz’s Adam Smith on the Labor Theory of Value

- Peter Foster’s Adam Smith Invisible Hand

- Marko Veckov’s Adam Smith on Labor Markets | Adam Smith Works

- Maryann Keating’s Adam Smith on Wage Taxes and Labor Force Participation

- Alex Aragona’s Adam Smith on the Interests of Labor and Business